In today’s world of pursuing excellence by being digitally innovative, central banks are following the global trend. Such digital innovation, known as CBDC, stands for Central Bank Digital Currency. The developed nations were also the first to experience it, and in December 2022, India too welcomed its ‘Digital Rupee’. As such, there have been considerable years when people, across the nation, were hooked on to digitally making their payments. This has been the main reason behind the introduction of the Digital Rupee. This digital currency launch is one of the significant steps taken by the Reserve Bank of India, which completely transforms how money is perceived, used for transactions, and managed. Even though digital currency presents certain challenges, the introduction of Digital Rupee presents multiple opportunities that signify India’s move towards becoming a digitally evolving nation.

What is Digital Rupee?

The Digital Rupee, also known as the e-Rupee (e₹), is a digital form of Indian currency issued by the RBI. It is often mistaken for being a form of cryptocurrency. However, unlike cryptocurrency, which is decentralised and operates without a central governing body, the Digital Rupee is a sovereign currency backed by the RBI. The key aim of introducing this digital currency is to complement the existing physical currency and offer an alternative to people that is secure, efficient and convenient to conduct transactions.

The pilot programme of the Digital Rupee was launched in December 2022. It is part of the broader initiative by the Indian government, along with the RBI, regarding modernizing the financial system and enhancing financial inclusion by promoting digital currency over physical cash. As the e-Rupee is issued as a legal tender by the RBI, it differs from the manner in which an individual holds deposits in bank accounts. It does not attract interest, which is generally accrued from conventional deposits. Yet, one’s deposits in the bank can be converted into digital rupees and vice versa.

Need for Digital Rupee

Rise of digital transactions

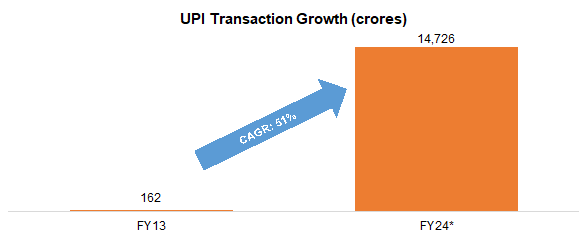

There has been a great rise in the volume of transactions conducted via digital channels as compared to conventional forms of transacting through physical banknotes ever since the UPI was launched. The RBI governor, in March 2024, announced that retail digital payments increased from 162 crore transactions in FY13 to over 14,726 crore transactions in FY24 (as of February 2024). He added that India now leads at the global level as it now accounts for ~46% of the world’s digital transactions.

Mass popularity of UPI is a result of India’s shift towards digitalization and a base for growth in the usage of the Digital Rupee. Mass appeal of UPI has also enabled dominating foreign players in the UPI space — such as Google Pay, Walmart-backed PhonePe and Amazon Pay — to enter the digital currency space. These companies own over 85% of India’s digital payments market share that takes place via UPI. Besides, for adding the facility of Digital Rupee on their portals they have tied up with RBI and NPCI. In doing so the company gets scope for more addition to the number of users along with flexibility to adapt the new entity called the Digital Rupee.

Financial Inclusion

India is an underdeveloped country and it is more dominated by villages in which majority population lives. It has been fighting with the challenge of financial inclusion. That’s why much of the population does not have any bank account due to lacking financial literacy and infrastructure. The infrastructural issues, backward connectivity, and socioeconomic constraints are the main reasons for low financial inclusion of the people residing in the rural region. As reported by RBI, India’s financial inclusion index stood at 56.4% as of March 2022. Digital currency can be made available in the rural sectors for bridging the gap because, with digital currency, it doesn’t necessarily demand fully operationalized bank accounts, and it is also available even in the absence of an internet connection. Therefore, smartphone usage and penetration levels are a prime enabler to adopt the adoption of digital currency.

A cashless economy will be encouraged.

Printing, distributing, and securing cash is a highly expensive affair for the government as well as financial institutions. The expense of printing currency notes between April 2021 and March 2022 was Rs. 4,984 crore (US$ 596.67 million), according to RBI reports. COVID-19 was an excellent example of cash mismanagement as cash was held as a precaution for the current challenges during that time. With the introduction of Digital Rupee, the costs involved reduce significantly and the need for holding physical cash diminishes. Additionally, it plays a big role in reducing the environmental issues that are caused in the process of printing and transporting cash.

Enhanced transparency and reducing fraud

Since CBDC is based on blockchain and similar technology, it increases the transparency of financial transactions. The scope for fraud and money laundering is reduced as each transaction can be traced and recorded.

Implementation of monetary policy

The current global economic crisis has a negative impact on the Indian financial system as well. During such periods, usually the RBI intervenes and manages the monetary policy. RBI makes sure that the steps taken help the financial condition of the country. Digital Rupee can help in such a situation as the RBI can issue or withdraw digital currency, and ultimately control money supply.

Impact of Digital Rupee

The introduction of digital currency is likely to have significant positive impact on the Indian economy. It will make payments faster, efficient, and secure. Some of the impacts of Digital Rupee in India on businesses and individuals are outlined below.

Impact on India

Digital Rupee is expected to benefit the Indian economy significantly and boost economic growth by enabling several factors such as:

- Increased financial inclusion

- Reduced cost of financial transactions

- Increased investments

- Increased economic growth

Impact on Indian businesses

The Digital Rupee is likely to make payment and receiving payments from customers and the other stakeholders conducting business in India easier for businesses. It is also expected to reap benefits to businesses by reaching new customers and expanding their markets.

Cost effective: Digital Rupee is likely to lower the cost of payment for companies. This is because digital rupee transactions are handled between wallets without involving intermediaries.

Operational efficiency: Since digital rupee transactions are processed in real time, 24/7, Digital Rupee is likely to make payments more efficient for companies.

Expanded markets: Since the acceptance of Digital Rupee payments is allowed anywhere in the world, this can be used as a method of expanding business and reaching out to more customers.

Impact on individuals

Digital Rupee is expected to positively impact the individual. It is likely to improve the convenience of individuals in making payments, saving money, and investing. It will also help them protect their money from fraud and theft. Here are some of the specific ways it is expected to impact individuals:

- Convenience in making payments

- Reduced risks of fraud and theft

- Financial inclusion

- Enhanced privacy

Conclusion

With the potential to change the way we make payments and manage our finances; the Digital Rupee is a new and modern form of currency. It is expected to have short- and long-term impact on the Indian economy and society. The Digital Rupee is still in the development stage. The Digital Rupee offers major scope in the areas of:

Cross-border payments

Innovation in fintech space

Integration with Blockchain technology

The Digital Rupee is not only another form of currency but rather a proof of innovation in the financial sector in India. With this new currency, India is presented with a chance to become a leader in the digital currency space.

Leave a Reply